The 1943 New York Standard Fire Policy and its Importance in Property Loss Settlement: A Perspective by John Knight, SLPA, MTPAI.

The New York Standard Fire Policy, known in the insurance industry simply as the NYSFP, is a document that defines the minimum coverages and rights of policyholders. The policy has been in use since 1943 and has been widely adopted by insurance companies across the United States and beyond. As a policyholder advocate, I believe that the NYSFP is a crucial tool in the settlement of property loss claims. In this blog post, I will explain why the NYSFP is so important and how it plays a vital role in ensuring fair and efficient property loss settlements.

One of the key benefits of the NYSFP is that it provides a clear and concise definition of what constitutes a covered loss. This helps to eliminate confusion and ensure that everyone involved in the settlement process is on the same page. For example, the policy defines what is meant by “fire” and “smoke damage,” which are two of the most common types of losses covered by fire insurance. This clarity is essential in ensuring that the insurance company and the insured are able to reach a fair and equitable settlement in the event of a loss.

Another important aspect of the NYSFP is that it sets out the responsibilities of the insurance company and the adjuster in the settlement process. The policy requires the insurance company to conduct a thorough investigation of the loss and determine the cause of the loss and to assess the extent of the damage.

The NYSFP defines key settlement options available to both the Policyholder and the Insurance Company; for example: 1. Appraisal, 2. The Insurance Company’s Option. Below I give the verbiage found in the NYSFP for each of these options.

There have been countless cases brought before the courts to settle disputes between policyholders and insurance companies over the wording in the NYSFP. Let me give you an example.

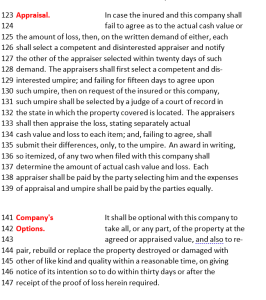

NYSFP APPRAISAL VERBIAGE “In case the insured and [the insurance company] shall fail to agree as to the actual cash value or the amount of loss, then,on the written demand of either, each shall select a competent and disinterested appraiser and notify the other of the appraiser selected within twenty days of such demand”.

NON-COMPLIANT APPRAISAL VERBIAGE “In case you and [the insurance company] shall fail to agree as to the actual cash value or the amount of loss, then you and [the insurance company] can submit the claim to appraisal”.

The NYSFP states that either the policyholder or the insurance company can invoke the appraisal clause. In instances where insurance companies have tried to limit the rights of policyholders by writing verbiage into the insurance policy requiring both the insurance company and the policyholder to agree to appraisal as a requirement of it being invoked, the courts have ruled that the insurance company verbiage affords policyholders fewer rights than those afforded by the NYSFP and have ruled in favor of the policyholders right to invoke appraisal on his/her/their own.

In conclusion, the NYSFP is a crucial tool in the settlement of property loss claims. It provides a clear and concise definition of what constitutes a covered loss, sets out the responsibilities of the insurance company and the policyholder, and provides a number of protections for policyholders. As a policyholder advocate, I believe that the NYSFP is essential in ensuring that property loss settlements are fair, efficient, and equitable. Every year our firm holds a week-long Master Training course for Public Adjusters from around the country. We believe that the NYSFP is such an important tool in claim settlement that we devote half of a day to discussing it with the adjusters who attend our Master Training Course.

If you have suffered a property loss, I encourage you to familiarize yourself with the provisions of the NYSFP and to work with a knowledgeable and experienced public adjusting firm or attorney who can help you navigate the settlement process.

Property Claim Advocates would be happy to discuss your claim with you. You can call and speak with me directly by calling 206-385-2172.

Written by John Knight and distributed by the Property Claim Adjustment Team at Claim Adjusters Network, LLC dba: Property Claim Advocates Mr. Knight is a Founding Partner of Claim Adjusters Network and a C.A.N University Master Trained Public Adjuster course instructor. Mr. knight has more than 25 years of well rounded experience in the insurance industry, including construction, mitigation, insurance appraisal, public adjusting, and teaching.

Fantastic blog post! I really appreciated your detailed explanation of the 1943 New York Standard Fire Policy and its significance in property loss settlements. Your insights were clear and informative, shedding light on this important topic. Thanks for sharing such valuable information!